HONG KONG, May 25 (Reuters Breakingviews) – Foreigners that once piled into offshore Chinese equities are evacuating as confidence in the country’s economic recovery sags. While concerns about President Xi Jinping’s agenda are valid, this wholesale flight looks hasty.

The China trade has always been unbalanced towards overseas-listed Chinese consumer and internet firms, and foreigners preferred building factories, acquiring large stakes in companies and the like over portfolio trading. Even at a peak in 2021, they held barely over 8 trillion yuan ($1.1 trillion) of yuan-denominated Chinese stocks and bonds, per official data, compared to $27 trillion of American equivalents. Now the former figure has fallen below 7 trillion yuan.

The offshore retreat has been even more dramatic. Hong Kong’s Hang Seng Index (.HSI) is down 4% this year and the Nasdaq Golden Dragon China Index (.HXC) of New York-listed mainland companies has lost twice that, having shed a whopping 70% of its value since December 2021.

That reverses a once-overcrowded trade that saw breathless Western investors pump up Chinese stocks in New York and Hong Kong to absurd levels. Luckin Coffee, for example, was a money-losing latte chain with a delivery app. Yet the company’s market value touched $12 billion in early 2020, equivalent to a lofty 23 times historical sales, before executives admitted to accounting fraud. Alibaba (9988.HK) and Tencent (0700.HK) alone have shed a combined $1 trillion in value from a peak in 2021. What appetite is left appears to be focused on state-owned telecommunication firms and banks: a craven flight to dubious safety.

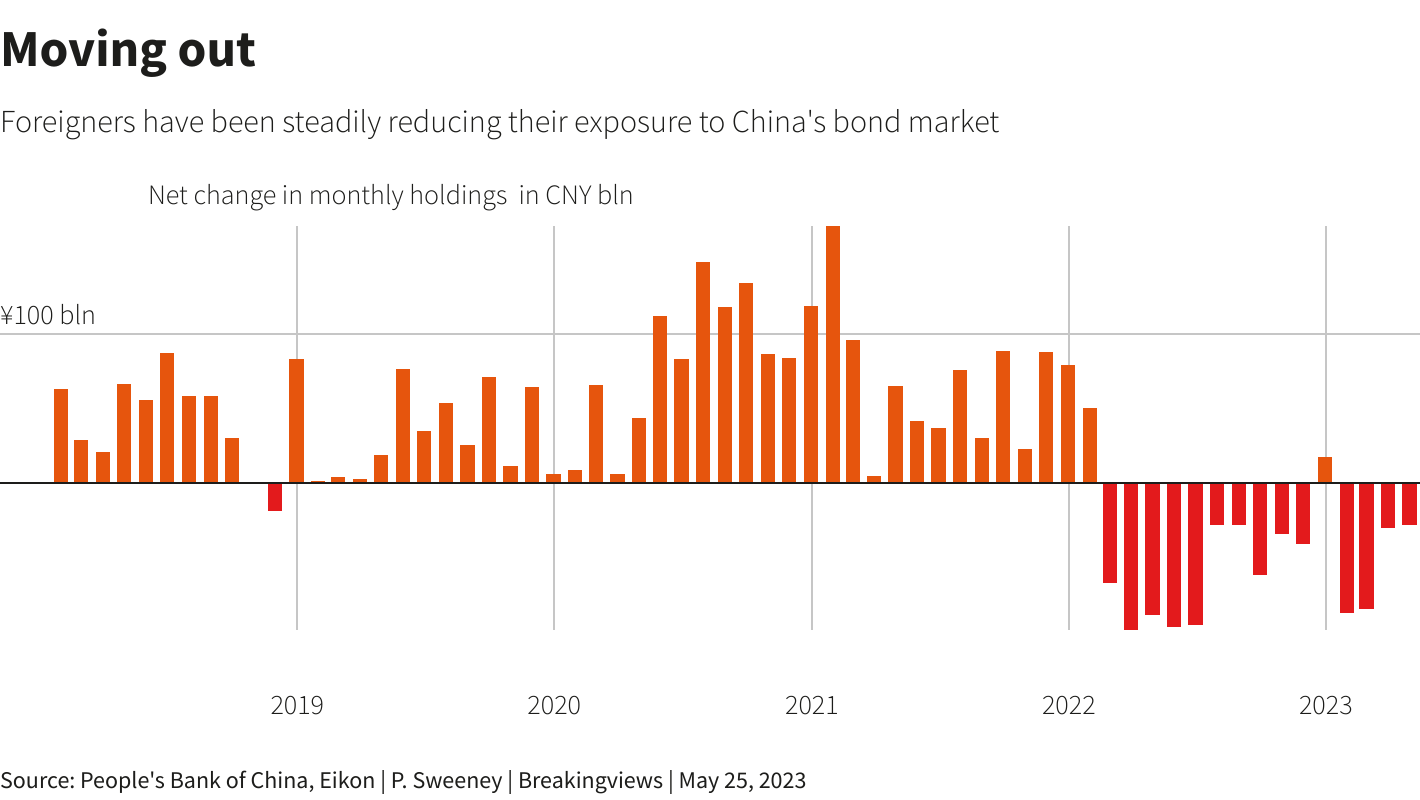

The loss of confidence extends to fixed income. With U.S. Treasury yields now higher than those on offer in the People’s Republic, overseas funds have moved out of sovereign and semi-sovereign bonds, while defaults by property developers and local government financing vehicles have scared most of them out of the corporate market.

To be sure, if war over Taiwan is imminent, or if Xi really plans to nationalise large parts of the private sector as some critics suspect, the People’s Republic is probably uninvestable. But there is a plausible alternative thesis: a new normal in which U.S.-China relations stabilise, consumption and real estate rebound and the second half of the year is better than the first.

That would offer an opportunity to selectively bargain-shop. For example, the average constituent on the domestic Chinese CSI300 Index (.CSI300) is priced at 27 times forward earnings, per Refinitiv data, yet those on the Hang Seng China Enterprises Index (.HSCE) trade at 8 times in Hong Kong. Hedge fund managers at the recent Sohn Investment Conference were bullish on vocational schools, hydropower and other stocks. Bond investors might also reconsider which government is more likely to default on its sovereign debt these days: Beijing or Washington? It is easier to assume the worst. It is also lazier and usually less profitable.

Follow @petesweeneypro on Twitter

CONTEXT NEWS

China’s benchmark CSI300 index tracking the largest listed firms in Shanghai and Shenzhen has slumped nearly 10% from a peak in January and is now flat for the year. Major Chinese indexes in Hong Kong and New York have also slid, with the Nasdaq Golden Dragon China Index having lost around 15% in the last three months.

Foreign positions in Chinese bonds have declined by nearly 880 billion yuan ($125 billion) between January 2021 and March 2023, central bank data shows.

The offshore yuan weakened past 7 per dollar on May 17 for the first time in five months amid signs that China’s post-Covid recovery is losing steam. April industrial output and retail sales growth undershot forecasts, leading multiple investment banks to adjust their expectations for China’s economic growth downward in response.

Our Standards: The Thomson Reuters Trust Principles.